Payment for cardiac surgery in Portugal is based on a contract agreement between hospitals and the health ministry. Our aim was to compare the prices paid according to this contract agreement with calculated costs in a population of patients aged ≥65 years undergoing cardiac surgery in one hospital department.

MethodsData on 250 patients operated between September 2011 and September 2012 were prospectively collected. The procedures studied were coronary artery bypass graft surgery (CABG) (n=67), valve surgery (n=156) and combined CABG and valve surgery (n=27). Costs were calculated by two methods: micro-costing when feasible and mean length of stay otherwise. Price information was provided by the hospital administration and calculated using the hospital's mean case-mix.

ResultsThirty-day mortality was 3.2%. Mean EuroSCORE I was 5.97 (standard deviation [SD] 4.5%), significantly lower for CABG (p<0.01). Mean intensive care unit stay was 3.27 days (SD 4.7) and mean hospital stay was 9.92 days (SD 6.30), both significantly shorter for CABG. Calculated costs for CABG were €6539.17 (SD 3990.26), for valve surgery €8289.72 (SD 3319.93) and for combined CABG and valve surgery €11498.24 (SD 10470.57). The payment for each patient was €4732.38 in 2011 and €4678.66 in 2012 based on the case-mix index of the hospital group, which was 2.06 in 2011 and 2.21 in 2012; however, the case-mix in our sample was 6.48 in 2011 and 6.26 in 2012.

ConclusionThe price paid for each patient was lower than the calculated costs. Prices would be higher than costs if the case-mix of the sample had been used. Costs were significantly lower for CABG.

O pagamento da cirurgia cardíaca é feito com base num contrato entre os hospitais e o ministério da Saúde. Comparámos o preço com o custo apurado num serviço específico, nos doentes com idade igual ou superior a 65 anos.

Material e métodosEstudo prospetivo entre setembro 2011 e setembro 2012 em 250 doentes submetidos a cirurgia de revascularização coronária (n=67), valvular (n=156) e coronária associada a valvular (n=27). Os custos foram apurados sempre que possível pelo método de microcusteio em alternativa pelo valor médio. O preço por doente foi facultado pela administração hospitalar, calculado usando o case mix médio do centro hospitalar.

ResultadosMortalidade aos 30 dias foi de 3,2%. Euroscore I médio foi 5,97 desvio padrão (DP) 4,50% significativamente inferior na cirurgia coronária. Tempo médio de UCI (3,27 DP 4,7), internamento total (9,92 DP 6,30) dias, ambos significativamente inferiores na cirurgia coronária isolada. Os custos apurados para cirurgia coronária foram (6539,17 DP 3990,26 €), valvulares (8289,72 DP 3319,93 €), valvulares com coronária associada (11498,24 DP 10470,57 €). Cada doente foi pago a 4732,38 em 2011 e a 4678,66 em 2012. usando o case mix do centro hospitalar que foi em 2011 (2,06) e em 2012 (2,17). O case mix da amostra foi 6,48 em 2011 e 6,26 em 2012.

ConclusãoO preço pago por doente foi inferior ao custo apurado. Caso tivesse sido usado o case mix da amostra, o preço teria sido superior ao custo. A cirurgia coronária é significativamente mais barata que a valvular.

The Portuguese National Health Service (NHS) was established in 1979, funded by the State budget, and hospitals were paid on the basis of historical costs. In the late 1980s the first steps were taken to assess the production of hospital services with the adoption of the system of classifying patients by diagnosis-related groups (DRGs), and in the early 1990s hospital funding moved to a contract system based on DRGs, but continuing to be allocated a budget rather than payment per episode.1 There are two main contract systems: retrospective, paid on the basis of previous expenditure; and prospective, based on the type, volume and price of the services provided, which can be calculated in advance.2

In recent years there have been attempts, not always successful, to reduce health care costs. New prospective funding models have been adopted in the European Union aimed at making management more accountable for the results obtained.3 The amount paid for services is established in advance, which encourages savings but introduces an element of uncertainty into the funding of health organizations.4 Payment for health care services provided by public hospitals to NHS patients is currently based on previously established contract agreements, but it is questionable whether payments made for patients for particular services, especially cardiac surgery, match the real costs at a state of efficiency.5

Patients may be overfunded or underfunded when different specialties are considered separately. It is thus important to analyze the differences between what cardiac surgery actually costs the NHS and the corresponding price that is established (perhaps artificially) in the hospital's funding model.

ObjectivesTo compare the price of cardiac surgery according to the contract agreement with calculated costs in one hospital department in a specific patient group – elderly patients (aged ≥65 years).

MethodsWe performed a prospective analysis of costs in patients undergoing cardiac surgery in a high-volume surgical center between September 2011 and September 2012. Patients aged ≥65 years who underwent elective coronary bypass graft surgery (CABG), valve surgery and combined CABG and valve surgery were included. Urgent procedures and reoperations were excluded. Subsequently, two patients who underwent a repeat procedure within a month were excluded despite initially fulfilling the inclusion criteria, as were another seven who were transferred to other hospitals, making it impossible to calculate costs.

The study was approved by the hospital's ethics committee and all included patients gave their written informed consent.

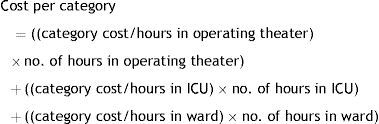

Costs can be calculated by different methods with different degrees of precision. The most precise method is micro-costing, which produces a unit cost, while the least precise is the mean daily cost of hospitalization. Analytical accounting uses mean daily cost for all categories of costs.6 Micro-costing, while probably better reflecting real costs, is more complicated and costly to apply to all categories of costs.6 We decided to use micro-costing for items for which it was feasible and provided information that justified the resources required for its calculation,6 while costs for other categories were calculated on the basis of length of stay in different sectors of the department (ward, intensive care unit [ICU] and operating theater).

Micro-costingThis method was used to calculate the costs of the following categories: diagnostic exams and medical acts, medications, transfusion products and surgical material. The number of medical acts provided for each patient in each category was obtained from the hospital's computer records and then multiplied by the corresponding unit cost. The unit costs of diagnostic exams and medical acts were taken from the price list set out in Order in Council 839-A/2009, the prices of transfusion products were provided by the hospital's hematology department, and the prices of medications and surgical material were obtained from the hospital administration.

Costing by mean length of stayMean values were calculated on the basis of the time the patient spent in each sector of the department, which was divided into three sectors: ward, operating theater and ICU.

A database was constructed in which the time each patient spent in each sector and the total costs per patient, per sector and for each of the following categories were recorded:

- 1.

Equipment (maintenance, compresses, syringes, needles, etc.)

- 2.

Hospital accommodation (clothing, cleaning, electricity, water, food, etc.)

- 3.

Personnel (physicians, nurses, technicians, auxiliaries, administrative staff).

The cost of each patient for each category was calculated using the following formula:

The costs for all patients were calculated in the same way, using micro-costing for certain cost categories and mean length of stay for others.

Payment methodThe method of payment for hospitals, set out in their contract agreements, is based on the total price of each line of production, using specific formulas for hospitalization, outpatient care, external consultations, emergency services, day care, chronic inpatient care and homecare.7 With regard to hospitalization, the most relevant to cardiac surgery, payment is made according to the following formula:

The number of equivalent patients for each DRG is calculated on the basis of the number of hospitalization episodes, obtained after conversion of days of hospital stay, episodes of exceptional duration, and patient transfers, into equivalent typical or normal episodes of that DRG.8 Normal hospitalization times have been defined for each DRG; a patient discharged following a normal or long hospitalization is considered an equivalent patient. Formulas supplied by the Central Administration of the Health System (ACSS) are applied in cases of short hospitalizations.9

The case-mix index is calculated as the number of equivalent patients multiplied by the relative weights of the respective DRGs, divided by the total number of equivalent patients. The national case-mix index for each year is, by definition, 1, but can be higher or lower in individual hospitals depending on the complexity of the patients treated.5,8 The base rate for each hospital group is calculated on the basis of unit costs per equivalent patient, using as the reference value the mean of the 30% most efficient hospitals in that group.5,8 The prices paid by the NHS in accordance with the contract agreement and the case-mix of our hospital and cardiac surgery department for 2011 and 2012 were supplied by the hospital administration.

Statistical analysisThe Kolmogorov-Smirnov test was used to test the normality of the variables of age, EuroSCORE I, and ICU and total hospital stay, with p values <0.05 considered statistically significant. The Kruskal-Wallis test was used to compare two or more samples of continuous variables and multiple one-way ANOVA if at least one of the samples was different. The latter two tests were used to analyze EuroSCORE I and ICU and total hospital stay for each procedure. These variables were chosen because they are directly related to greater complexity and potentially higher costs. Multifactorial regression was used to analyze costs including the explanatory factors of gender, age, type of procedure, EuroSCORE I and proportion of hospital stay in the ICU.

ResultsThe final population consisted of 250 patients. Table 1 shows their gender distribution, functional class, comorbidities and type of procedure.

Gender distribution and clinical and procedural characteristics of the study population.

| No. | % | ||

|---|---|---|---|

| Gender | Male | 129 | 51.6 |

| Female | 121 | 48.4 | |

| Angina (CCS class) | I | 135 | 54 |

| II | 87 | 34.8 | |

| III | 28 | 11.2 | |

| IV | 0 | 0 | |

| Functional class (NYHA) | I | 18 | 7.2 |

| II | 112 | 44.8 | |

| III | 120 | 48 | |

| IV | 0 | 0 | |

| Hypertension | Yes | 231 | 92.4 |

| No | 19 | 7.6 | |

| Hypercholesterolemia | Yes | 210 | 84 |

| No | 40 | 16 | |

| COPD | Yes | 20 | 8 |

| No | 230 | 92 | |

| Creatinine >2 mg/dl | Yes | 5 | 2 |

| No | 245 | 98 | |

| Smoking | Current | 6 | 2.4 |

| Ex-smoker | 58 | 23.2 | |

| Non-smoker | 186 | 74.4 | |

| Ejection fraction | Good (>50%) | 201 | 80.4 |

| Reasonable (30-50%) | 46 | 18.4 | |

| Poor (<30%) | 3 | 1.2 | |

| Procedure | CABG | 67 | 26.8 |

| Combined CABG and valve | 27 | 10.8 | |

| Valve | 156 | 62.4 |

CABG: coronary artery bypass graft surgery; CS: Canadian Cardiovascular Society; COPD: chronic obstructive pulmonary disease; NYHA: New York Heart Association.

Mean age was 74.22 years (SD 5.58), median 74.0. Thirty-day mortality was 3.2%. Predicted in-hospital 30-day mortality according to EuroSCORE I was 5.97 (SD 4.50), median 4.81.10,11 EuroSCORE I for patients undergoing combined coronary and valve surgery was 7.12 (SD 4.45), significantly higher than the 3.89 (SD 4.71) for those undergoing isolated CABG (p<0.001) but not significantly different from the 6.66 (SD 4.14) for isolated valve surgery (p=0.807). Mortality in valve surgery patients was significantly higher than for CABG patients (p<0.001).

Hospital stayMean ICU stay was 3.27 days (SD 4.7), median 2.00 days. It was significantly longer in combined CABG and valve surgery patients (5.89 days [SD 10.47], median 2.00) and in isolated valve surgery patients (3.06 [SD 3.09], median 2.00) than in isolated CABG patients (2.72 [SD 3.8], median 2.00) (p<0.05). There was no significant difference between isolated valve surgery and combined CABG and valve surgery (p=0.35).

Mean hospital stay was 9.92 days (SD 6.30), median 8.00 days. Mean hospital stay of valve surgery patients was 9.87 (SD 5.45), median 8.00, and was 13.70 (SD 11.51) for combined CABG and valve surgery patients, significantly longer than for CABG (mean 8.51 [SD 4.47], median 7.00) (p<0.05). There was no significant difference between isolated valve surgery and combined CABG and valve surgery (p=0.61).

CostsTable 2 shows the costs per procedure and per cost category.

Costs per procedure and per cost category (in euros).

| CABG | Valve | CABG and valve | Mean | |

|---|---|---|---|---|

| Medication | 182 (SD 777) | 135 (SD 192) | 559 (SD 1351) | 193 (SD 624) |

| Surgical material | 1631 (SD 324) | 3101 (SD 699) | 3421 (SD 776) | 2741 (SD 925) |

| Diagnostic exams and medical acts | 1694 (SD 1584) | 1602 (SD 1251) | 2606 (SD 3479) | 1735 (SD 1731) |

| Blood products | 336 (SD 456) | 465 (SD 580) | 735 (SD 802) | 460 (SD 587) |

| Personnel costs | 1529 (SD 954) | 1694 (SD 859) | 2397 (SD 2616) | 1726 (SD 1214) |

| Equipment | 833 (SD 587) | 903 (SD 457) | 1252 (SD 1610) | 922 (SD 711) |

| Hospital accommodation | 331 (SD 192) | 386 (SD 217) | 525 (SD 507) | 387 (SD 262) |

| Total | 6539 (SD 3990) | 8289 (SD 3319) | 11498 (SD 10470) | 8166 (SD 4945) |

CABG: coronary artery bypass graft surgery.

Table 2 reveals that the cost categories of surgical material, diagnostic exams and medical acts and personnel costs account for around 75% of the total costs. The total costs do not have a normal distribution (p<0.05), which is explained by the fact that eight patients incurred extremely high costs. After eliminating these patients and performing a logarithmic transformation of the variable “costs”, the normality of the transformed variable cannot be rejected (p>0.05). A multifactorial regression can then be performed with the logarithmically transformed dependent variable “costs” and the explanatory factors of gender, age, type of procedure, EuroSCORE I and proportion of hospital stay in the ICU.

The results show higher costs for female gender (p<0.05), but no association between age and costs (p>0.05). Regarding type of procedure, isolated CABG incurred lower costs than valve surgery or combined CABG and valve surgery (p<0.05). EuroSCORE I only had predictive value (p<0.1) in the sense that higher scores were associated with higher costs, while a greater proportion of hospital stay in the ICU was significantly associated with higher costs (p<0.05). The variance explained by the model was 33%, and there were therefore other factors that significantly influenced costs which were not included in the model. The importance of extreme values should be noted in the effect of longer stays in the ICU, which considerably increased overall costs. Of the cost categories, surgical material accounted for the largest proportion of total costs, and the variance explained by this category is therefore greater than the other categories. Age was associated with higher personnel and equipment costs (p>0.05), while EuroSCORE I showed no association with any cost category. Combined CABG and valve surgery was associated with higher costs in all categories, while isolated valve surgery incurred higher costs than CABG in surgical material, equipment and hospital accommodation. A greater proportion of hospital stay in the ICU was associated with higher costs in all categories except hospital accommodation.

PricesWe then calculated the prices paid for the patients in our sample, based on values for 2011 and 2012 stipulated in the contract agreement provided by the hospital administration. In 2011 the hospital's case-mix index was 2.0572 and in 2012 it was 2.2107. The base rate was €2300 in 2011 and €2116 in 2012. Payment for each cardiac surgery patient was thus €4732.38 in 2011 and €4678.66 in 2012.

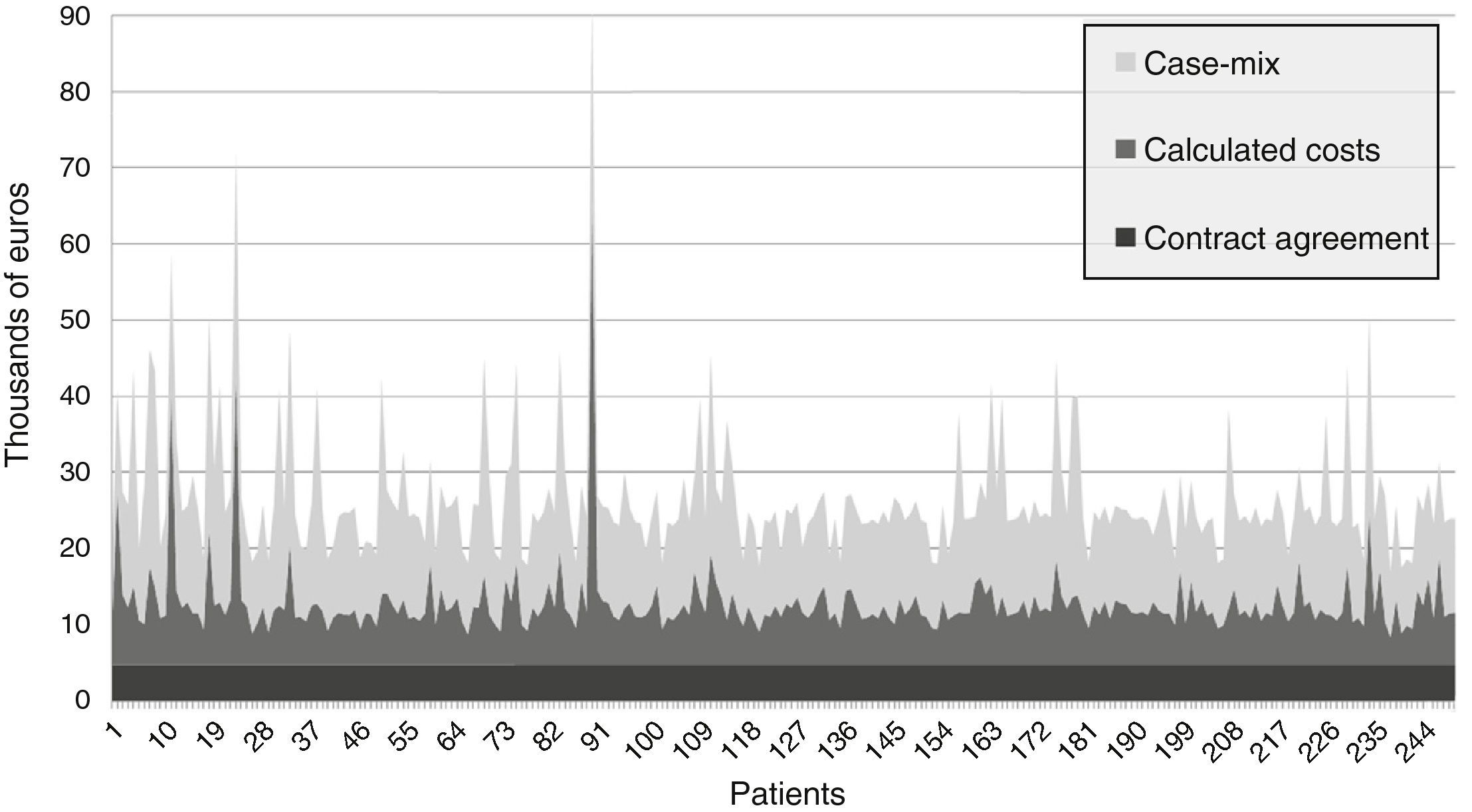

Considering that the mean case-mix of our patients was 6.4761 (SD 2.72) in 2011 and 6.2618 (SD 2.13) in 2012, and using the same base rates, the prices adjusted for complexity would be €14895.03 (SD 6254.42) in 2011 and €13249.97 (SD 4518.33) in 2012 (Figure 1).

The price paid according to the contract agreement was lower than the calculated costs for all patients in the study, while the complexity-adjusted price was well above the calculated costs for all patients. Consequently, if payment were made per DRG episode (the base rate payment), costs would be completely covered. Since prices paid under the contract agreement are substantially lower than the costs, cardiac surgery is a net contributor to the underfunding of the hospital.

DiscussionIn this study we compared the calculated costs in a cardiac surgery department with the payments made according to the hospital's contract agreement. The procedures under analysis were isolated CABG, isolated valve surgery and combined CABG and valve surgery, in patients aged ≥65 years. Calculated costs were broken down into seven categories: medication, surgical material, diagnostic exams and medical acts, blood products, personnel, equipment and maintenance, and hospital accommodation. Calculations were based on micro-costing for categories in which this was feasible and on mean length of stay otherwise. The mean overall calculated cost per surgery was €8166.29 (SD 4945.18). Certain variables were associated with higher costs in certain categories: female gender (higher costs for diagnostic exams), type of procedure (combined CABG and valve surgery, the most complex, incurred the highest costs in all categories, while valve surgery was more costly in terms of surgical material, equipment and hospital accommodation than CABG), and a greater proportion of hospital stay in the ICU (higher costs in all categories except hospital accommodation).

The calculated costs were considerably lower than those reported in published studies, most from the US, and were closer to those seen in European hospitals.12–14 Studies have reported a mean cost of €29000 for CABG15 and €28000-€40000 for aortic valve surgery in the USA.12,16 The prices paid for cardiac surgery vary widely between American centers, and in most cases are higher than in Europe, although higher prices do not produce better results, and so health authorities in the USA are seeking to lower prices to the levels of those in the least expensive centers.17

The price paid per patient in our hospital was €4732.38 in 2011 and €4678.66 in 2012, whereas the mean calculated cost in our sample was €8166.29 (SD 4945.18). It may thus appear that the cardiac surgery department has a negative impact on the hospital's budget, but this is not in fact the case. The hospital's case-mix index was 2.0572 in 2011 and 2.2107 in 2012, while in our sample it was three times higher, 6.4761 in 2011 and 6.2618 in 2012. If the case-mix used to calculate prices were that of our patients, the prices to be paid would be €14895.03 per patient in 2011 and €13249.97 in 2012, well above both the payment made and the calculated mean cost. The same amount was paid for all the patients in our sample. Our analysis shows that payments for more complex patients should be calculated differently, as shown by the fact that costs for combined CABG and valve surgery were higher in all categories.

Risk should also be a consideration when calculating prices, since our study reveals a tendency for higher EuroSCORE I to be associated with higher costs. Clinical performance, although known to affect costs, was not considered in this study. Nevertheless, the fact that predicted mortality was 6%, while actual mortality was around half of this (3.2%), demonstrates good clinical performance, similar to the best centers, which report mortality that is half of that predicted by EuroSCORE I.

Since the Portuguese NHS is funded almost entirely by the state budget, and is thus under government control, a funding system could be implemented that included changes in the coding of DRGs, took patient complexity into consideration, and indexed results to risk. This should be borne in mind when considering changing the status of some departments to that of responsibility centers, since funding needs to take account of the complexity of the patients treated. This thinking also underlies the contract agreement system and is already applied to different types of hospital group but, unfortunately, not yet to different departments.

It is hard to tell whether the frequent claims that the health system is underfunded are entirely true. What we do know is that funding does not take full account of differences in the complexity of practices. If every department were funded in accordance with the complexity of its cases, the volume of its activity and its performance, the discrepancy between prices paid and costs incurred would not be so striking. Ideally, funding would take into account not only complexity but also performance, as shown by clinical outcomes and efficiency, often now jointly defined as effectiveness. The difference between prices and costs, which would in this case be much less than seen in our study, would ideally function as an incentive (or disincentive) for managers, but we are still far from such a situation. Our aim is not to argue as to which funding system to adopt but to take full advantage of the existing system, which, if the will is there, can ensure that payment is in line with performance.

LimitationsWhen calculating costs, we did not include indirect costs, including those resulting from patients’ inability to work and care provided by families. The patients in our study population were aged ≥65 years and had thus reached retirement age, and their inability to work could therefore not be included in the costing, while the costs to patients’ families were not included because they are difficult to quantify and account for only a small proportion of the total costs. Certain fixed costs were also excluded, such as the acquisition of equipment like ventilators, initial installation costs and property costs, as well as the fixed costs of the hospital administration, which would be hard to calculate. However, we have provided a detailed description of the methods used, thus enabling comparison with other centers.

ConclusionThe prices paid for cardiac surgery in accordance with the contract agreement were considerably lower than the calculated costs. This difference may to some extent be artificial, since cardiac surgery is funded according to the hospital's case-mix and not according to the case-mix of patients in the department. Costs for patients undergoing CABG are significantly lower than those undergoing valve surgery, which suggests that prices should be higher for more complex patients.

Ethical disclosuresProtection of human and animal subjectsThe authors declare that no experiments were performed on humans or animals for this study.

Confidentiality of dataThe authors declare that no patient data appear in this article.

Right to privacy and informed consentThe authors have obtained the written informed consent of the patients or subjects mentioned in the article. The corresponding author is in possession of this document.

Conflicts of interestThe authors have no conflicts of interest to declare.

We thank Nurses Alda Catela and Dário Antunes for their assistance in collecting and processing the data for this study.

Please cite this article as: Coelho P, Rodrigues V, Miranda L, Fragata J, Pita Barros P. Serão preço e custo coincidentes na cirurgia cardíaca do idoso? Rev Port Cardiol. 2017;36:35–41.